While the global economy had gotten used to nearly a decade of low or near zero interest rate policy, things have changed since late 2015 when initial signs of a global economic recovery alongside a nascent pick-up in inflation pushed the Fed to delicately hike the short term fed funds rates by 25 basis points. Back then, investors were quite skeptical on the pace of the global recovery that many speculated that the Fed would sooner than later start cutting rates again. However, with a second interest rate hike done with and the central bank likely to follow through with its decision on three rate hikes in 2017, the threat of rising interest rates have suddenly become real.

Investors are now caught with not just the interest rate risk but also the threat of rising inflation. Latest readings from the U.S. department of commerce showed that the consumer price index was sitting comfortably above the Fed’s 2% inflation target rate. Furthermore, with the unemployment rate near the Fed’s full employment threshold, there is little evidence or reason for the Fed not to hike rates.

The changes in the monetary policy, which has long been coming now exposes the risks of rising interests rate, but investors have often found different ways to hedge the risks of interest rates. In this article, we look at five ways how interest rate hikes can be hedged.

1. Sell bonds to hedge against rate hikes

The simplest way to hedge against a raising rate hike environment is to sell bonds that an investor already has. Of course, despite being simple this is also the most drastic or an extreme step. However, investors can then use the proceeds from the bond sales and invest the same into an interest bearing account or put the proceeds into a money-market fund that could appreciate from a rate hike.

This extreme step is ideal when the pace of rate hikes are significant and in the same note, it is unlikely that the U.S. Federal Reserve will embark on a significant rate hike policy as its decisions could have far reaching implications in this day and age. Still, a rapid pace of policy tightening is not unheard of and is quite prevalent among emerging economies. For example, the Mexican central bank, Banxico has been raising rates.

Just between November 2016 and February 2017, the Mexican central bank hiked rates by nearly 100 basis points and this was just a small part of the wider page of rate hikes which the central bank was involved in since early 2016.

Although the odds of a similar scale of rate hikes from the Fed is very low, the examples from Mexico and from other central banks includes Bank of Russia during the peak of the Ukrainian tensions shows that central banks do not hesitate when it comes to the pace of rate hikes or even rate cuts.

In the U.S., we already have evidence where in 1973, inflation in the nation nearly tripled from 3.9% to 9.6% which prompted the Fed to hike rates from 5.75% to as much as 11%, nearly double. With the Fed falling behind the curve, the pace of rate hikes was fast. Inflation in the U.S. continued to rise at a strong pace into early 1975, which saw the central bank playing catch up. Interestingly, rates started being cut right after as well.

The chart below shows a glimpse of the pace of rate hikes and cuts between the periods of 2001 and 2006.

2. Use short duration ETF’s to hedge against rate hikes

When the Fed signals a rate hike, there is no doubt that bond yields rise across the curve. The short end of the yield curve is the most influenced however by the Fed funds rate. A potential increase in the 30-day Fed funds rate can push the yields on the 2-year, 5-year and the 10-year Treasuries quite significantly. For investors who want to protect against the increase utilizing ETF’s is a great way to hedge or even minimize the impact of higher interest rates or even better, being able to take advantage of the Fed funds rate hikes.

Investors can look at some bond related ETF’s such as the lower duration bonds. During rising interest rate environments, it is ideal for investors to reduce the duration on the bonds that they hold. This is measured as an interest rate hike which is based on the bond’ maturity and the coupon payments. It is not hard to see why holding a higher duration bond carries larger interest rate risk compared to a short bond duration portfolio. A shorter bond duration portfolio can be quickly built up by investing only in short term bonds. While this is a great way to hedge the risks of a rate hike, on the flipside, the short term bonds tend to give smaller yields as well.

With ETF’s investing in bonds is easy as one can easily switch between short term and long term duration bonds according to the changing landscape. Some of the notable short term duration bonds include the iShares 1 – 3 year Treasury Bond ETF (SHY) and the PIMCO Enhanced Short maturity Active ETF (MINT), which are one of the most widely used ETF’s to hedge against the Fed funds rate hike or the interest rate hike.

When picking Bond Exchange Traded Funds investors should bear in mind that the Treasuries on the longer end of the yield curve are less influenced by the Fed rate hikes and more influenced by inflation. Thus, despite the Fed hiking rates, if bond investors do not see an evidence of inflation, the yields on the longer dated bonds tend to remain low. Therefore, when looking at the various bond ETF’s that are available for trading, investors should focus only on the very short term bond ETF’s, in other words; ones that are no longer than 2-years in maturity as these type of ETF’s tend to be the most vulnerable to the Fed funds rate decision.

3. Treasury Inflation-Protected Securities

TIPS as they are commonly called are one of the most widely talked about securities when it comes to protecting against rate hikes. However, on closer observation, TIPS are more suited to protect against rise in inflation than interest rates. But with rising inflation, interest rate hikes aren’t far behind, which puts TIPS securities as either being half full or half empty. Still, whether TIPS are a hedge against inflation or against interest rate hikes, the fact remains that TIPS remain a big part of the hedging tool against the Fed funds rates.

TIPS are a recent addition, only available since late 1990. TIPS are vastly different from the regular or nominal bonds such as the Treasury bonds, although they are the same in terms of the coupon payments or the par value. While traditional Treasuries do not account for inflation, TIPS do, meaning that if a traditional Treasury has a coupon payment of 5%, but inflation is running at 1.5%, then the real yield is only 3.5%. If inflation continues to rise, the real yield continues to fall.

TIPS, on the other hand guarantee’s that the principle value will rise along with inflation, measured by the Consumer Price Index. Therefore, TIPS coupon payments reflect the real yield, accounting for inflation, thus indirectly accounting for the rate hikes as well. This is of course assuming that interest rate hikes and inflation move in tandem, which is not always the case.

There are different TIPS ETF’s that investors can look at, with the iShares TIPS Bond ETF being one of them. The chart below shows the TIPS ETF historical NAV.

4. Hedging the Fed funds rate with Treasury futures

Treasury futures have been trading on the CME since 1976 and tracks the underlying security which is the Treasury Bill, Note or the Bond. When rates hike (starting with the short term Fed funds rates) the prices of the Treasuries fall. Thus, long positions on the Treasury futures contracts are ideal to profit from rising bond prices, which means a falling interest rate regime. Likewise, futures traders can short the Treasuries to profit from the falling prices, which means rising yields or higher interest rates.

There are many different treasury futures contracts one can choose from. Some of the most ideal Treasury futures contracts to trade are the T-Bill futures. These futures come with the February, March, April, June, September and December delivery. The T-Bill futures are listed in the International Monetary Market (IMM) index calculated as 100 minus the discount yield. Thus, if the price of a $100 90-day T-bill was $98.00, then the IMM equals 92. The T-bills come with a 0.005 tick size which is equal to $12.50 or $25 for a full basis point.

Besides the T-bill futures, other contracts include the Eurodollar. These are the deposits denominated in a currency other than the home currency. While the eurodollar futures are more liquid contracts compared to the T-bill futures, they are also very volatile.

5. Bank stocks as a hedge against rising rates

Banking stocks tend to perform better during an interest rate hike cycle and thus the Fed funds rate hike is an ideal environment. Banks make business by the net interest income, which is the different in the interest charged on loans and the interest paid on deposits. When interest rates start to rise, the interest income starts to grow faster as the interest charged on the loans is higher.

Despite the Fed funds rates or the short term rates rising, the rate at which the commercial banks hike interest rates on deposits is lot a slower. Thus, the pace of rate hikes on deposits is not the same as that on loans, which puts the bank at an advantage. Furthermore, banks also make use of funding from institutional investors to supplement the deposit base and these investments are often structured such that they are minimal on the effects of interest rate changes. There are also referred to as the interest rate swaps which are derivates instruments used to stabilize the interest rate expenses even further.

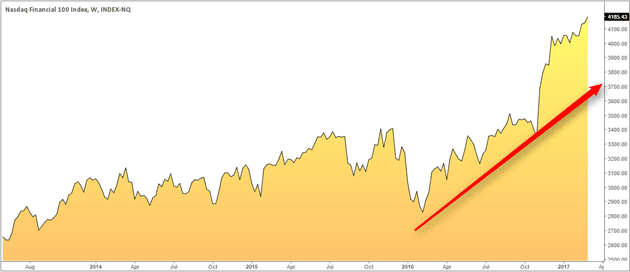

The chart below shows the Nasdaq Financial 100 index (IXC) which shows significant increase since 2015 – 2016 as the pace of rate hikes started to increase and expectations of further rate hikes started to fuel the rally in the financial index.

Therefore, a good way to hedge against interest rate risk is to look at the banking stocks, with a focus some of the top-notch banks. Besides banking stocks other financial firms that deal with lending or financing can also benefit from a rising interest rate regime.

The above methods outlined are just some of the ways investors can look at hedging the Fed funds rate or the short term interest rates. For those who prefer to have a more direct approach with the Fed funds rate, the 30-day Fed funds futures contracts are as close as one can get. With enough liquidity, short term traders are at a distinctive advantage to be positioned to capitalize on the short term fluctuations in the interest rates.

However, as with any futures contracts, traders should be aware of potential risks on the 30-day fed funds futures contracts as these tend to be set by market forces and not the other way around. Meaning that a slight distortion or even a hint of doubt on whether the Fed will hike rates at the next upcoming meeting could significantly push prices around. Thus, a trader needs to be very cautious when trading the 30-day fed funds futures especially on plans to leave the positions open overnight.

From an investor’s perspective care should be taken so that proper decisions can be made rather than making haste. There are many examples where the markets have turned bullish on rate hikes in the first few months following a rate hike decision only for these expectations to be scaled back drastically. Therefore, investors should focus not just on the Fed’s decision to hike rates but also on inflation expectations.