In this post, we will uncover the pros and cons of interchange fees legislation in the United States and around the globe.

The policy conversations were in full swing from 2005 with the initial filing from consumers to the final judgment in 2011. We will walk you through the early days of the litigation and bring you forward to today.

Why is this important to you?

Well, it can impact the costs banks pass on to you the consumer in the future, so it’s great to have an understanding of the laws on the books.

2005 – 2011

The new law known as the Durbin Amendment reduced the interchange fees for debit transactions to a flat 12 cents instead of the ~1.14% average fee of the sales price. In typical fashion, the banks found other ways to recoup these potential losses.

Even though Republican Congresswoman Shelley Moore introduced legislation on March 16, 2011, to delay the Durbin Amendment until a comprehensive study could be performed, banks went on the offensive. JP Morgan Chase announced on Monday, March 21, 2011, that they will no longer offer debit-card rewards for the majority of its customers in July of that year.

The elimination of the debit-card rewards program by Chase was reported by Bloomberg. The July cutoff is no coincidence as the flat interchange fee becomes law on July 21, 2011.

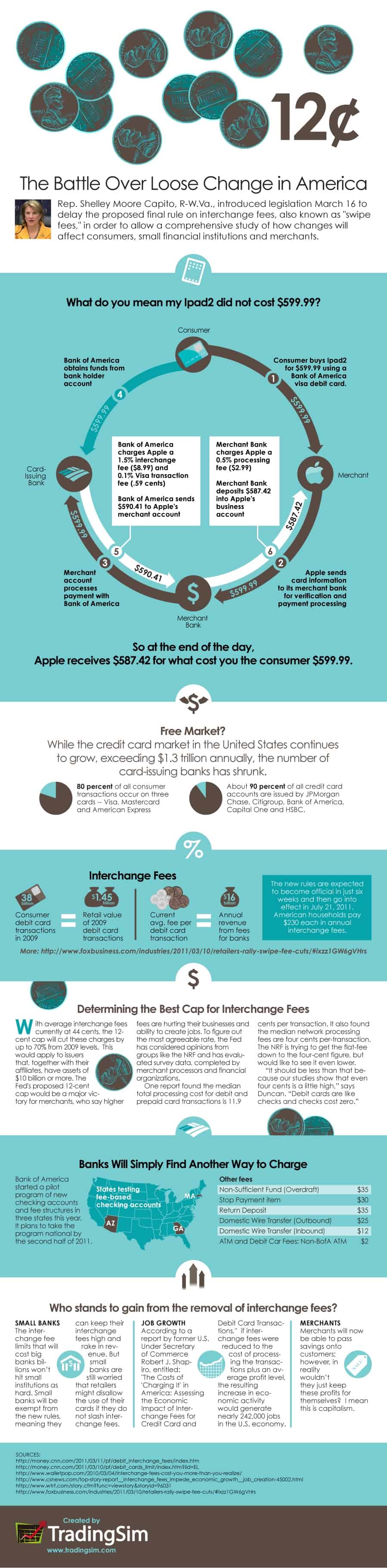

The below infographic provides both sides of the story. On one hand, there are people that believe the reduction in fees will lead to cost savings for the consumer. In 2003, Australia removed interchange fees and there was no uptick in the economy or reduction of goods and services.

In actuality, many Australians complain that prices stayed the same, while they did see an increase in banking fees, loss of free checking, and the elimination of debit-card rewards programs.

Interchange Fees Infographic

Wow.

Lots of bad data. I bet that Apple pays HALF that in merchant account fees. Whomever created this, probably a student or a teacher, has either bad information or is flat out lying about certain fees and the structure of how bankcard fees are really handled.

Aesthetically pleasing, yes, however very incorrect, dangerously incorrect even.

The interchange rates are in large part made up of risks. One major risk is the cost of credit card and debit card fraud. The Durbin legislation comes in at a time when technology is able to reduce a substantial portion of this risk of card duplication. With the introduction of the PIN and chip technology duplication has now become much harder requiring a level of technology that is much higher than the technology required to copy magnetic strips.

So while the banks lost revenue prediction are probably valid here, it’s the drop in cost of transaction that will maintain the banks profitably as this new card technology along with newer POS terminals get introduced.

I think the banks profit for this service will probably rise to new levels within the next few years.